/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

Ever since artificial intelligence (AI) became the buzzword in 2023, Nvidia (NVDA) has been at the forefront of the AI trade. NVDA stock gained 239% in 2023 and another 171% in 2024. Last year’s price action was more muted by that yardstick, as the stock rose only 39%. Those returns should be seen in perspective, however — Nvidia not only outperformed the S&P 500 Index ($SPX) by a decent margin but was also the second-best-performing “Magnificent 7” stock, trailing only Alphabet (GOOGL), which saw a rerating of sorts last year.

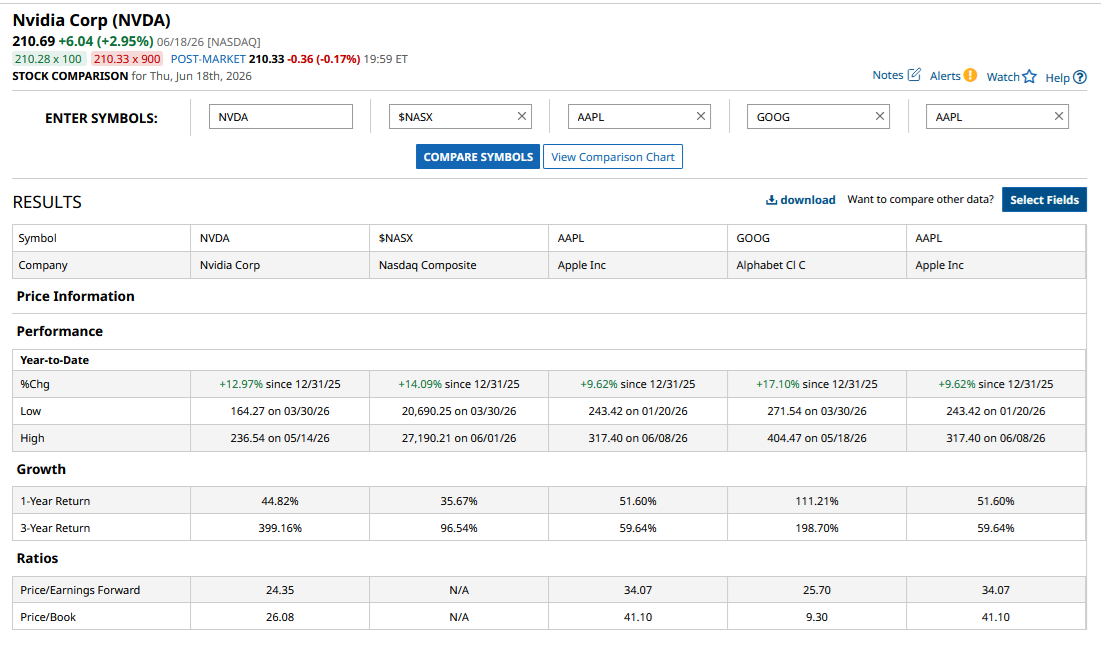

Nvidia Is Underperforming the Nasdaq Composite in 2026

Cut to 2026, and we see something similar. Alphabet is still the best-performing Mag 7 stock, followed by NVDA stock. However, while GOOGL stock’s year-to-date (YTD) returns are slightly ahead of the Nasdaq Composite ($NASX), Nvidia is trailing the tech-heavy index. Needless to say, the remaining Mag 7 stocks are also underperforming the index this year.

For the last few months, I have been arguing that it would be folly to expect NVDA stock to double every year, and investors should temper their expectations. The stock has been moving like a normal stock, which I contend is actually not a bad thing.

Nvidia Is No Longer the Frontline AI Stock

Notably, Mag 7 stocks — Nvidia included — are no longer the favorite AI plays for investors. We now have SpaceX (SPCX), which has projected itself as more of an AI giant rather than a rocket and internet connectivity company. Even Cathie Wood — a steadfast Tesla (TSLA) bull — sold some TSLA shares to make way for SpaceX (SPCX).

The AI trade has transitioned from the Magnificent 7 to memory companies whose shares have skyrocketed this year. Other companies in the chip ecosystem, like Advanced Micro Devices (AMD), Lam Research (LRCX), and Applied Materials (AMAT), are also among the top S&P 500 gainers this year, along with Intel (INTC), which deserves a special mention. The once-iconic U.S. chip giant was fighting a survival battle until about a year ago, and its shares tumbled to multi-year lows. However, a series of developments fueled a more than 600% rally in INTC stock from its 2025 lows.

NVDA Stock Forecast

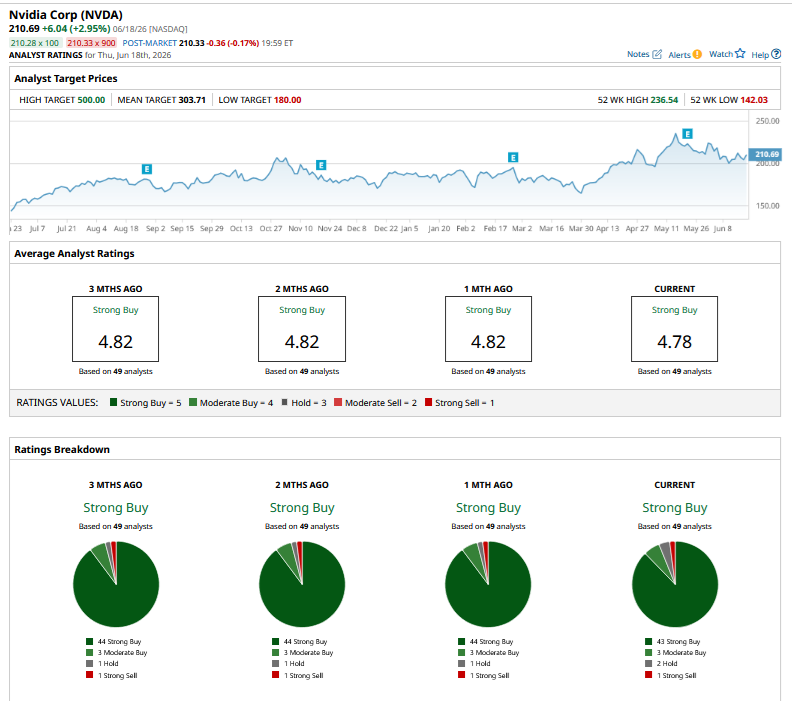

Meanwhile, although Nvidia has been out of favor with the markets, brokerages continue to be in love with NVDA stock and have been gradually raising their target prices. After the company’s fiscal first-quarter 2027 earnings last month, Benchmark raised its target price from $250 to $335, while Evercore raised its target from $352 to $413.

Baird analyst Tristan Gerra raised his price target from $300 to a Street-high of $500. If Nvidia stock were to hit this mark, the company’s market capitalization would soar past $10 trillion.

How Should You Play Nvidia Stock Now?

Nvidia trades at a forward price-to-earnings (P/E) multiple of 24.3 times, while the P/E-to-growth (PEG) multiple is 0.47 times. Usually, such multiples for a high-growth and quality name like Nvidia would be mouthwateringly cheap, as it's not often we find companies of this caliber at a PEG below 1 times.

However, markets have been worried about Nvidia for two main reasons. The first is, of course, apprehension over the sustainability of AI capex over the medium to long term. Since the bulk of Nvidia’s revenue now comes from AI chip sales, its earnings are highly susceptible to any slowdown in AI capex. Second, there is growing competition in the AI chip market, including from players like Amazon (AMZN) and Alphabet, which happen to be among Nvidia’s biggest customers. These companies are not only using their chips internally, which means less reliance on Nvidia chips, but also actively seeking third-party customers, competing with Nvidia in the process.

While these concerns are genuine, I believe they are overblown. The AI capex frenzy is far from over and is, in fact, getting broad-based beyond the hyperscalers. Nvidia has incidentally started reporting its data-center segment into two sub-markets — AI Clouds, Industrial, and Enterprise (ACIE), and Hyperscale — signaling the growing importance of non-hyperscalers.

Nvidia has also expanded its target market by another $200 billion with central processing units (CPUs) and expects $20 billion in revenue from CPUs this year alone. Sovereign AI and physical AI are also compelling stories and should help keep Nvidia’s growth buoyed over the next few years. I continue to stay bullish on Nvidia given its reasonable valuations and see NVDA stock ending this year with significant gains, albeit not to the extent that we saw between 2023 and 2024.